In short

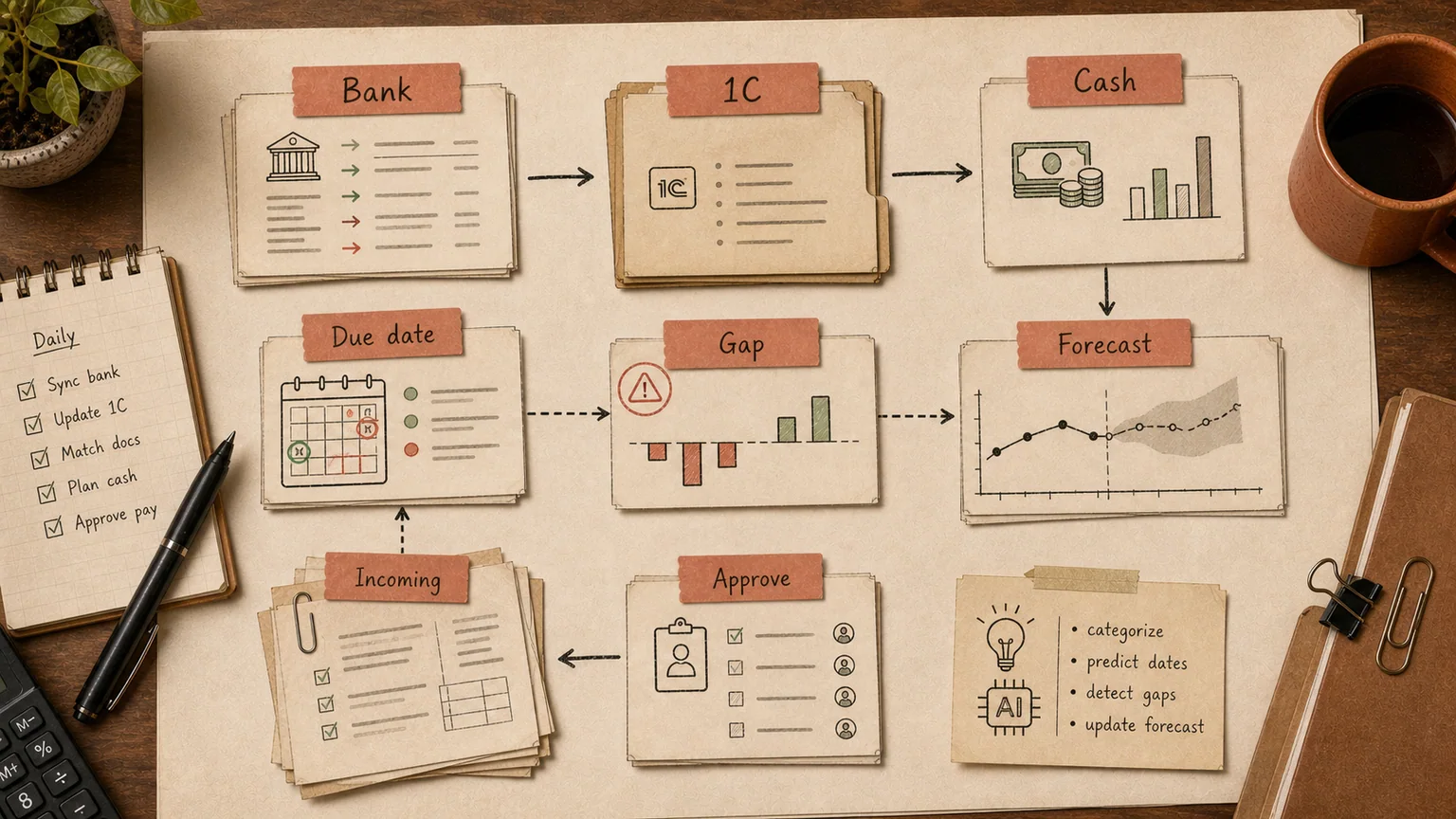

A payment calendar is a day-by-day view of expected cash in and cash out: which invoices should get paid and when, which bills are due, and what the account balance looks like on each date in between. It is a narrower, more operational cousin of a 13-week cash flow forecast. Most finance teams start it in a spreadsheet, and a spreadsheet is fine until the business runs enough vendors, customers, and bank accounts that someone has to update it by hand every single day to keep it honest.

AI does not replace the treasury function here. It replaces two things a spreadsheet is bad at: pulling transaction data from multiple accounts and systems into one place, and predicting when a customer will actually pay instead of trusting the date printed on the invoice. The decision about which payment to delay or accelerate still belongs to a person.

What a payment calendar actually tracks

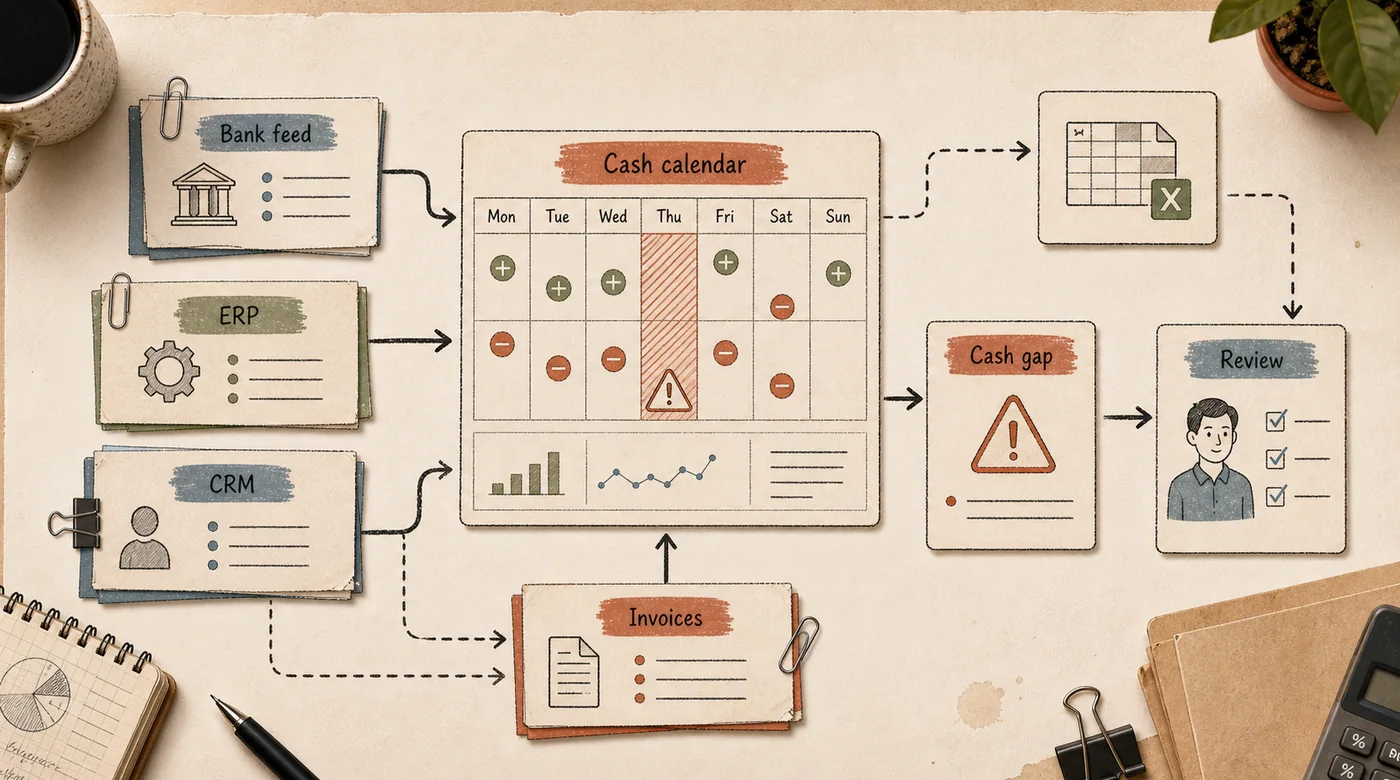

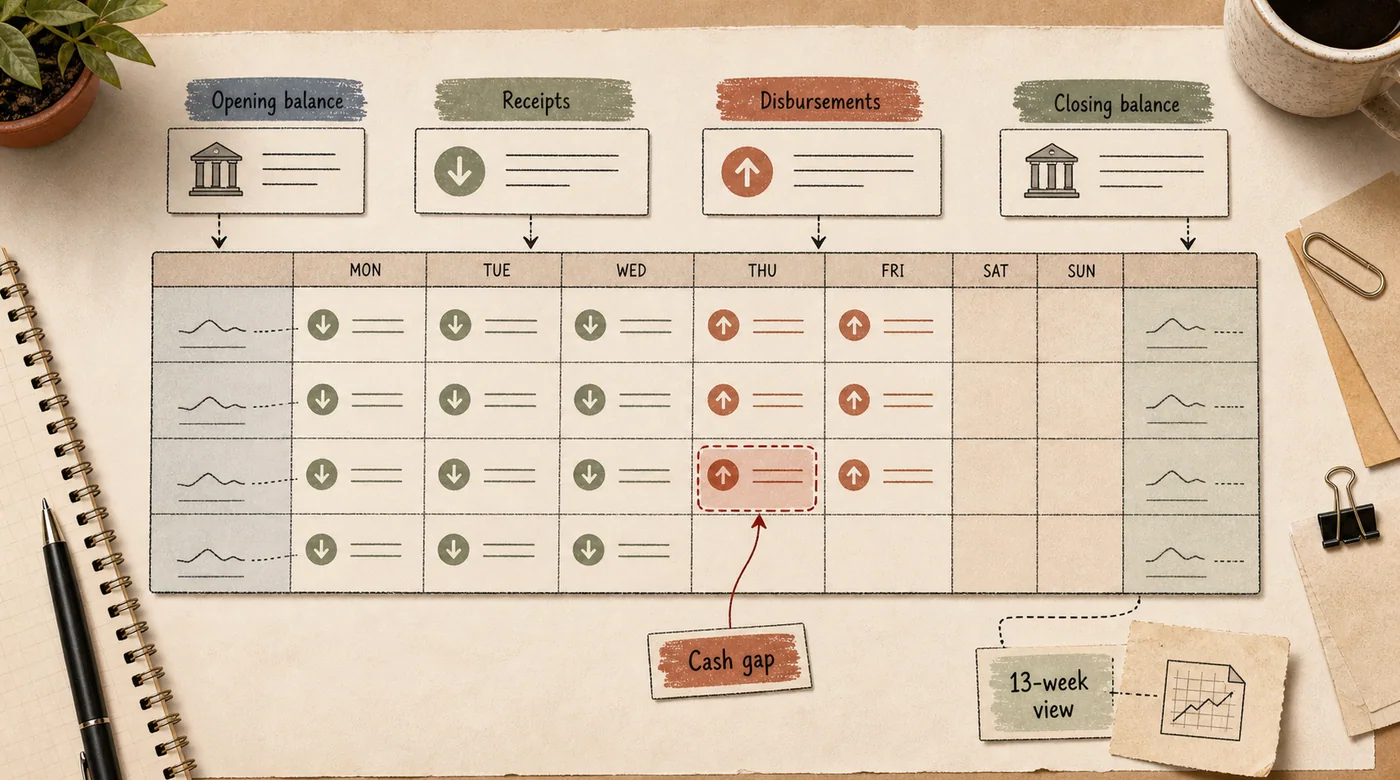

The calendar answers one question: will there be enough cash in the account on a given day once every expected inflow and outflow is accounted for. It is different from a P&L. A company can be profitable this quarter and still miss payroll on the 5th because a large customer paid two weeks late. The structure is simple: opening balance, expected receipts (customer payments, draws on credit lines, other income), expected disbursements (vendor payments, payroll, taxes, rent, debt service), closing balance. A closing balance that goes negative is a cash gap, and the whole point of the calendar is to surface that gap weeks before it happens, not on the morning AP can't clear a payment.

Treasury teams running a rolling 13-week cash flow forecast are solving the same underlying problem at a slightly longer horizon. Best practice there is to expect roughly 90-95% accuracy in weeks one through four and let accuracy degrade naturally further out — the payment calendar is the short end of that same curve, where precision matters more because the horizon is days, not weeks.

Where spreadsheets and ERP modules break down

A spreadsheet payment calendar works fine at low transaction volume with one person maintaining it. The failure mode is always the same: someone has to manually export a bank statement, reconcile it against open invoices and bills, and fold in new requests from other departments — every day, without missing anything. In practice that discipline slips. The file gets updated every two or three days, and by the time a gap shows up on screen, there is no time left to react to it.

ERP systems do better on one axis: the payment calendar draws from the same sales orders, purchase invoices, and payment terms already in the system, so at least the plan is internally consistent. But ERP modules are strong at "what should happen per the contract" and weak at "what will actually happen." They rarely account for the fact that a specific customer reliably pays 7-10 days late, or that another one pays early if nudged. A lot of real cash movement also happens outside the clean document trail: ACH payments a controller adjusts manually, early payment discounts negotiated informally, or deposits a salesperson forgot to log.

The second failure point is multi-entity consolidation. Once a company has several bank accounts, subsidiaries, or business units, and payment activity flows through different banking portals and merchant processors, reconciling a single picture by hand becomes a Friday-afternoon ritual that is stale again by Tuesday. Most CFOs still describe the actual bottleneck as manually exporting CSVs and copy-pasting them into a master sheet — not a lack of forecasting theory.

What AI actually automates here

AI is not useful for "make the spreadsheet look nicer" — a normal report already does that. It earns its keep where scattered, imperfect data needs to become a usable forecast. In most stacks this is a matter of connecting a model to systems you already run rather than buying a separate platform finance has to maintain on its own.

Predicting the real payment date. Instead of trusting the invoice terms, a model looks at each customer's payment history: average days late, seasonality, whether delays are chronic or occasional. The output is not "due on the 15th" but a probability-weighted range — most likely the 15th-20th, with a confidence level attached. That range surfaces a gap earlier than a single hard date ever could.

Pulling data out of every source. Bank feeds, ERP exports, CRM payment status, a vendor invoice sitting in an inbox as a PDF — a model can read and reconcile these into one stream without someone re-typing numbers. This is the same underlying capability behind a good AI document assistant: not replacing the controller, just removing the manual re-entry between systems that don't talk to each other.

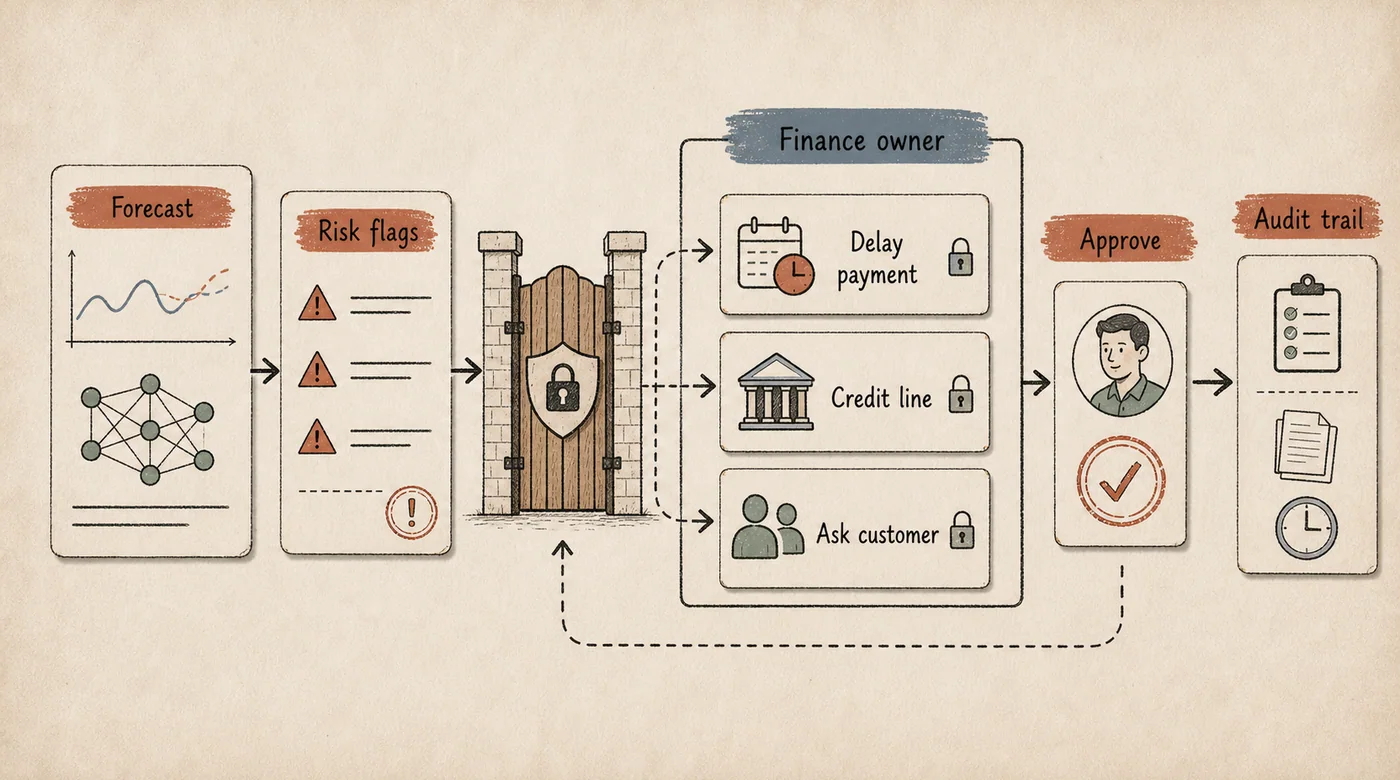

Flagging risk early, not just gaps. A model can scan the calendar four to eight weeks out and highlight not only a hard negative balance but a risk zone: balance close to zero, a large vendor payment landing the same week as an unconfirmed customer receipt. The output a CFO actually wants is a short list of the three or four days worth checking first, not a fully recalculated spreadsheet.

Scenario drafts. "What happens if customer X pays two weeks late" or "what if we push a vendor payment by a week" are usually modeled by copying a tab and hand-editing formulas. AI can draft that scenario in minutes. The decision to actually delay a payment stays with a human, because delaying has consequences a spreadsheet doesn't capture: vendor relationships, penalty clauses, and reputation.

Answering questions in plain language. Instead of hunting through a wide export for the right column, a controller can ask "what do we owe vendors next week" or "which customers are chronically more than 10 days late" and get an answer against current data, not a file from last Monday.

What AI should not do in a payment calendar

A model should not decide unilaterally which payment gets delayed or prioritized when cash is tight — that is a judgment call with legal and relationship consequences, and it stays with the CFO or controller. It also should not be the system of record for the actual account balance; the bank feed is the source of truth, the forecast is a layer on top of it. And a payment-delay probability is a signal to look closer, not a basis for treating a customer as delinquent — that distinction matters especially with long-standing accounts that have a legitimate, if slow, payment pattern.

Input data quality sets the ceiling here. If invoices get entered a week late or a chunk of payment activity never makes it into any system, no model fixes that — it trains on an incomplete picture and produces confident, wrong forecasts. Before trusting a forecast with real payment decisions, it is worth testing it the way you would test any AI system with evals: known-late payers, disputed invoices, seasonal customers, and the edge cases that break a spreadsheet formula just as easily.

What this looks like in practice

A mid-market company running several bank accounts and business units typically has one or two finance staff manually reconciling bank feeds against the payment calendar every morning. Gaps get caught one or two days out, which leaves almost no room to maneuver beyond an emergency credit line draw or a call to a key customer asking them to pay early.

Once a forecasting layer sits on top of the existing ERP and bank feeds, using actual payment history per customer instead of contract terms, the visibility window typically stretches to two or three weeks. The finance team does not lose control over who gets paid first — that decision stays put — but it stops spending hours every week reconciling spreadsheets by hand.

The same gap between "we technically have AI access" and "the finance team actually uses it to check numbers" shows up in training as much as in tooling. Teams build the habit of verifying a forecast against a live invoice or bank line faster when corporate AI training works off their own transactions and vendor files instead of a generic demo dataset.

Running a pilot without replacing your accounting system

There is no need to connect AI to every account and entity on day one. A reasonable first step is to scope one segment — accounts receivable for a single business unit or region where cash gaps happen most often — and give the model twelve months of payment history, the bank feed, and current open invoices. Compare its forecast against what actually happened over four to six weeks before expanding to other accounts or entities.

Decide early who reviews the flagged risk days each morning and who has authority to approve a payment delay. Without a clear owner, even an accurate forecast turns into a report nobody opens.

How to tell the pilot worked

Three practical signals: the horizon at which a gap becomes visible stretches from a day or two to two or three weeks; the finance team spends hours, not days, reconciling data each week; and the number of emergency moves — a rushed credit line draw, a call asking a customer to pay early — drops over a quarter. If the controller still double-checks every number by hand after rollout because they don't trust the source data, the problem is data quality, not the model, and that has to get fixed before the system expands further.

FAQ

Is a payment calendar the same as a 13-week cash flow forecast?

Not quite. A 13-week forecast plans over a longer horizon with less daily granularity, usually rebuilt weekly. A payment calendar operates at the day level, over a shorter window, where the exact date matters more than the aggregate total for the period.

Do we need to replace our ERP or accounting system?

Usually not. An AI forecasting layer typically sits on top of the existing ERP and bank feeds rather than replacing the system of record.

Where should we start if everything still lives in a spreadsheet?

Pick one segment — one business unit or one AR portfolio — and pull twelve months of payment history first. That lets you validate forecast accuracy before expanding scope.

How long does a first pilot take?

Four to six weeks is usually enough to compare the model's forecast against actual payments and decide whether to expand it.

If the payment calendar in your company is a spreadsheet someone rebuilds every week, the fix usually isn't a more complex tool — it's a forecasting layer on what you already have, measured by how many extra days of warning it buys you before the next gap.