In short

Kaspi QR is how most retail payments happen in Kazakhstan: the merchant opens a code inside the Kaspi Pay app, the customer scans it with the Kaspi.kz app on their own phone, and confirms the charge in two taps. No card reader, no card data typed anywhere. Funds land in the merchant's account within one business day, and the standard fee is 0.95% per transaction.

If you are building payment flows, marketplace integrations, or point-of-sale software for the Kazakhstan or CIS market, Kaspi QR is not optional background context - it is the default rail your customers already expect, the way Alipay is in China or PIX is in Brazil. This piece breaks down how it works, where it differs from a card terminal, and what a foreign team building on top of it usually gets wrong the first time.

Why Kaspi QR exists and why it won

Kazakhstan's card-present retail market never had a mature multi-acquirer terminal network the way Western Europe or the US did. Kaspi filled that gap directly with a bank-owned super-app: one login for payments, marketplace shopping, and lending. The QR mechanism works because Kaspi already controls both sides of the transaction - the merchant account and the customer's stored card - so a scan-and-confirm flow replaces card-present authorization entirely.

The result is a closed-loop system. Bloomberg reported that Kaspi opened its QR rails to more third-party participants only as the central bank pushed for broader interoperability - before that, QR volume ran almost entirely through Kaspi's own app. For a payments product manager, the practical read is: assume most Kazakhstan consumers already have Kaspi installed, and assume merchant adoption is closer to universal than niche. Nearly every retail counter, cafe, and market stall in the country displays a Kaspi QR sticker.

That is a different adoption curve than most Western QR pilots, where merchants had to be convinced to add a code next to an existing terminal. In Kazakhstan the QR code often came first.

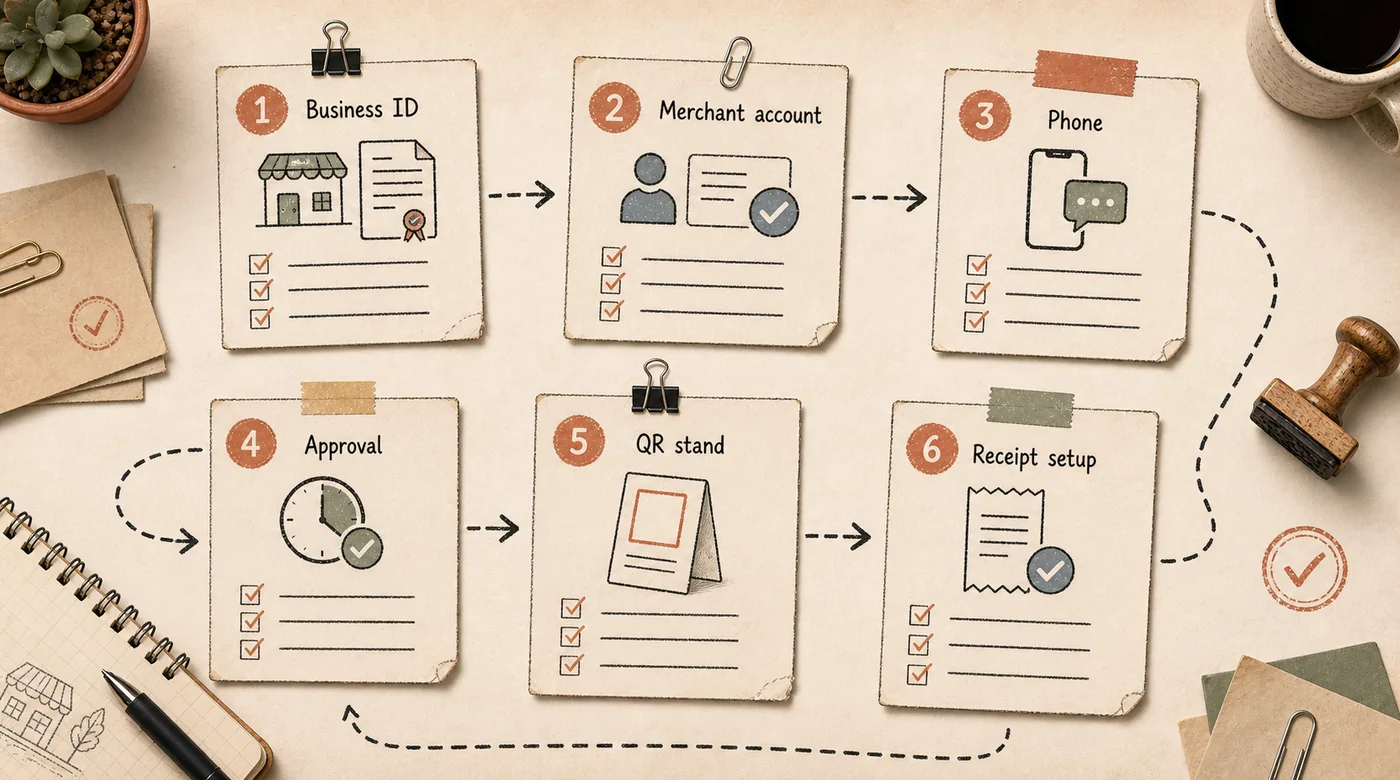

How merchant onboarding works

A business owner opens the Kaspi.kz app, registers a Kaspi Pay merchant account against their business registration (an ИП sole-proprietor or a ТОО, the local LLP equivalent) and a Kazakhstani phone number. There is no branch visit and no hardware order. A freshly registered business typically has to wait a few business days for the tax registry sync before the merchant account activates; an existing business can usually get approved same-day.

The fee structure has two parts that are easy to conflate: a 0.95% transaction fee on QR and remote payments, and a separate flat account-service fee of roughly 1,950 tenge a month (about $4). New merchants get a fee-free window in the first months, which is a useful detail if you are modeling unit economics for a Kazakhstan expansion and comparing it against a Stripe or Adyen cost base - the account fee is trivial, but it is not zero, and some teams forget to model it.

Kaspi QR versus a POS terminal

These get bundled together in casual conversation, but they are different products with different reach.

Source: the official guide.kaspi.kz Kaspi QR page, public page captured in July 2026.

Kaspi QR alone is app-only: a code with or without a preset amount, shown from the merchant's phone. It handles payments from Kaspi Gold balances and Kaspi's in-house credit products. It cannot take a Visa or Mastercard issued by a different bank, because there is no card reader in the flow at all.

Kaspi POS - either a physical Smart POS unit or the phone-based Mobile POS mode inside the same app - adds card-present acceptance for other banks' cards, alongside QR and cash reconciliation. The QR-and-remote fee stays at 0.95%, but card and installment-credit transactions are priced differently by merchant category, and that rate can run well above 1% in some categories.

For a product team scoping a Kazakhstan launch: if your target segment is consumer retail where most shoppers already bank with Kaspi, QR-only acceptance covers a large share of transactions with zero hardware cost. If your buyers are more likely to hold cards from other regional banks, or you need card-present fallback, budget for POS hardware from day one rather than treating it as a later add-on.

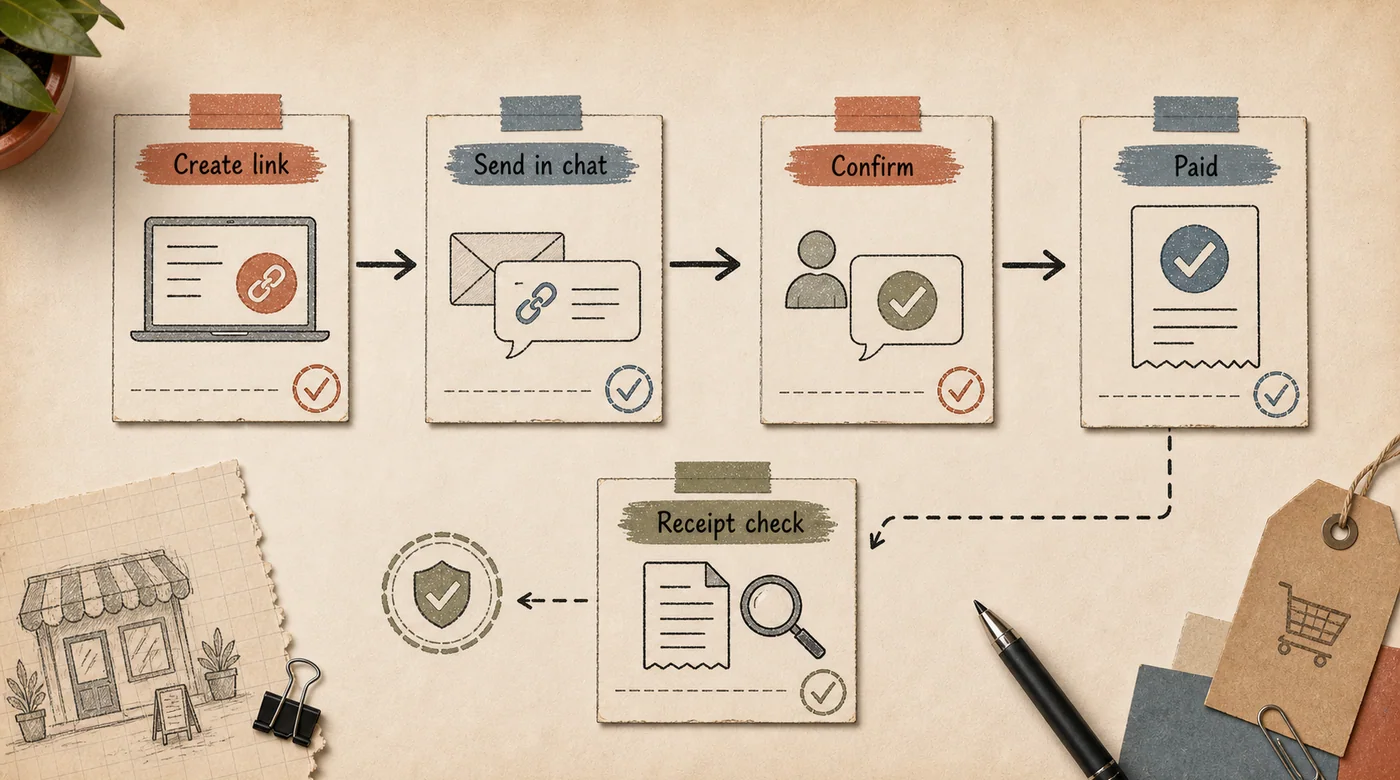

Remote payments: the no-terminal use case

Kaspi Pay also supports invoice-style remote payment links, generated from the merchant app and shared over messaging apps or posted in an Instagram bio. The customer opens the link, sees the amount, and confirms in their own Kaspi.kz app - useful for delivery businesses, service providers who take deposits before a booking, and any seller without a fixed physical counter. The fee is the same 0.95%, with no separate "remote" surcharge.

This pattern matters for anyone building a checkout flow that targets Kazakhstan customers from outside the country: a payment link generated inside a merchant's own app, rather than a hosted checkout page you control, is the default mental model local buyers already have.

Receipts and tax compliance

One detail that trips up foreign-run businesses and marketplaces operating in Kazakhstan: a fiscal receipt is legally required for essentially every sale to a consumer, and accepting payment through Kaspi QR does not remove that obligation. The payment method and the fiscal receipt are two separate compliance layers under Kazakhstan's tax code.

Merchants running Kaspi Kassa (Kaspi's own fiscal cash register software) get receipts generated automatically the moment a QR, credit, or remote payment clears, delivered straight to the buyer's Kaspi.kz messages. Merchants without that integration still have to issue a receipt through whatever certified cash register they already use for cash sales - Kaspi does not fiscalize the sale on its own outside that ecosystem. If you are building software that automates order fulfillment on top of Kaspi payments, this is the step teams most often skip in a first release, and it is the one a Kazakhstan tax audit checks first.

What to build first if you're integrating

Most integration work does not start with the payment rail itself - Kaspi's merchant app already handles that reliably. It starts with the reconciliation layer: matching a Kaspi payment notification to an order, a customer, and a receipt, across however many sales channels the business runs. Teams that skip this step end up with a spreadsheet stitching together Kaspi Pay history, a fulfillment system, and a fiscal cash register that don't talk to each other.

A minimal first build usually needs: a webhook or polling layer that picks up confirmed Kaspi payments, an order-matching rule (amount plus timestamp plus channel, since Kaspi payment references are not always rich), and a reconciliation view so a shop owner is not manually cross-checking three apps. If your business already runs on a sales dashboard or lightweight internal tool, that is usually the fastest place to plug Kaspi payment status in, rather than building a standalone payments admin panel from scratch. This is really a narrow instance of a broader question worth answering first: how to bring AI into a small operation without over-tooling a team that just needs fewer manual steps.

FAQ

Does Kaspi QR work for a business without a Kazakhstan bank account?

No. A Kaspi Pay merchant account requires local business registration (ИП or ТОО) and ties to the Kazakhstan tax registry. A foreign company selling into Kazakhstan typically needs a local entity or a local partner to accept Kaspi QR directly.

Is the 0.95% fee negotiable?

Not for standard merchant accounts opened through the app - it is a flat published rate, not something a support call adjusts. Lower or different rates apply only to specific partner programs or business categories that Kaspi manages directly.

Can Kaspi QR payments be automated end-to-end without manual reconciliation?

Yes, but it takes a webhook or API layer on top of the merchant account rather than relying on the Kaspi Pay app UI alone. That integration work is usually where a real build effort goes, not the payment acceptance itself.

Does Kaspi QR work offline?

No. Both the merchant's code and the customer's scan-and-confirm step require an internet connection - this is not an NFC or offline tap-to-pay technology. A weak signal at checkout is a common failure mode worth testing for before launch.

If your product already accepts Kaspi payments but reconciliation still runs through spreadsheets, that is usually the next thing worth fixing before adding another payment method.